How Strong Is the U.S. Economy

An Unbiased Appraisal

Deciphering the state of the U.S. economy is an intriguing challenge, given the polarizing views we hear daily from various sources. On one hand, there's a narrative of prosperity; on the other, there's a narrative of impending doom. This dichotomy engages our curiosity and prompts us to seek a balanced perspective. To understand this issue, we consult our unbiased credit markets, where people put money, not politics, to work to settle this question.

Bonds with a Single-B rating for corporations are deemed to be highly speculative investments that offer a higher yield to compensate investors for the higher risk of default. These yields tend to rise when a recession is in progress or when one is approaching, as credit market investors begin to worry that in a weak economic environment, vulnerable companies will likely encounter problems servicing their debt. Single-B credit rating yields (as compiled by Bank of America) peaked at 22.7% (weekly average) during the global financial crisis, GFC (in Nov. 2008) when the U.S. experienced a deep recession.

Research by SP Global reveals that the 3-year cumulative default rate for B-rated (below investment grade) companies is 12.41%, compared to 0.91% for BBB-rated (investment grade) firms. Since the risk of default increases/decreases during recessions/expansions, credit market participants look to these yields to see how financial markets are gauging the risk to the U.S. economy. Not surprisingly, high-yield bonds tend to see yields moving higher during recessions while they move lower during economic expansions. This can be observed in the chart below, where the shaded areas represent actual U.S. recessions.

Today, single B credit yields are hovering at 8.02%, higher than the 7.40% rating at the end of 2023 but quite distant from its previous peak of 22.7% during the GFC. Still, some credit analysts focus on high-yield credit spreads, representing the difference between single B credit yields and the 10-year Treasury yield. Such yields remain well below readings observed in prior U.S. recessions.

In a recent in-person client presentation, I was challenged to show data for each recession for the Bank of America data series (starting in 1997) to see how the latest reading compares to prior recessions.

As one can see, despite the 62-basis point rise in the high-yield credit spread from the end of last year, the current high-yield spread is lower than any other recession (including the averages for a recession) in Bank of America’s data set.

Other individuals in the presentation asked whether I could compare the current high-yield credit spread to previous economic expansions to explore the vulnerability of our current economic expansion. The results revealed that lower high-yield credit spreads suggest U.S. credit markets are less worried about a recession today than in prior expansions.

What is Wrong with the U.S. Economy Today?

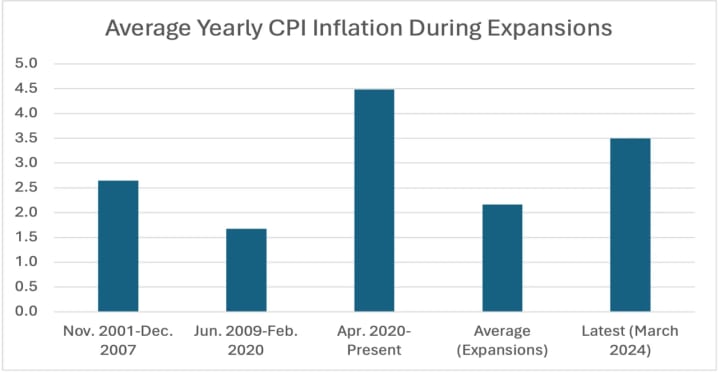

This week, in another client presentation, one participant in the audience did not like my research results and challenged me to find things wrong with the current expansion. I said a straightforward response would center around our inflation problem!

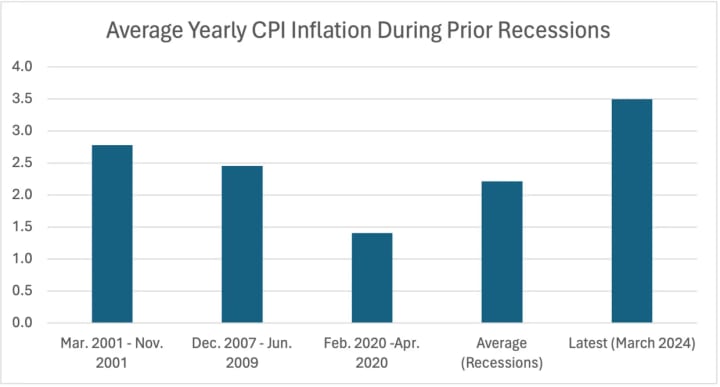

My analysis reveals that the yearly Consumer Price Index (CPI) increases have averaged 3.5% in the current expansion, compared to an average reading of 2.2% during prior economic expansions in our sample period. I will leave it up to the reader to decide if the cause of this malaise is due to the Russian-Ukraine crisis, which some say boosted food and energy prices, the global Covid-19 pandemic, which some argue pumped massive amounts of money into the economy as production came to a standstill and led to demand-pull inflation or simply due to bad economic policy from the current administration.

Inflation is also higher than we have typically observed during recessions. Well, I am thrilled to report that I left some people happy in my latest economic presentations because even though the data revealed that credit markets are still perceiving the risk of an immediate recession as relatively low, they were thrilled that I found some evidence supporting the view that something is wrong with the current economic expansion, namely higher than average inflation!

Summary and Concluding Thoughts

Some individuals have been telling us that a recession has been ongoing since 2021, while others have stated that the current expansion has been performing like the Ever-ready Bunny without any hesitation. SIFMA (Securities Industry and Financial Market Association) estimates that $1.3 trillion is traded daily in U.S. Fixed-Income securities. With such sums, there should be little doubt that profit incentives rather than political bias determine high-yield credit spreads.

The bottom line is that the U.S. credit markets tell us that no recession is within our immediate horizon. However, things could change in a New York minute if the economy experiences a shock like a broader escalation of the war in the Middle East between Iran and Israel, which boosts the price of oil to over $125.00 per barrel, or whether the Russian-Ukraine conflict was to escalate and lead to higher food and energy prices. In short, for all those hoping to see a collapse in the U.S. economy soon, many black swans are lingering around, which could provide the shock that the U.S. economy needs to slip into a recession and make their wishes a reality! Since 1957, the year I was born, a recession has occurred on average every 5.7 years and we all know the last recession ended in April 2020.

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Enjoyed the story? Support the Creator.

Subscribe for free to receive all their stories in your feed. You could also pledge your support or give them a one-off tip, letting them know you appreciate their work.

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

What is Holding Back the Federal Reserve?

Analysts and investors typically use two popular methods to predict when the Federal Reserve will begin an easing cycle. The first tracks the movements in proxy variables for the Fed’s dual mandates: seeking sufficient employment growth and stable inflation growth. The second approach tracks the statements made by Fed talking heads for clues on when they will begin to lower interest rates. Given the wide dispersion of Fed comments (weighted by the relative importance of each respective Fed official offering their perspective), forecasting policy moves can be challenging. Of course, an alternative path is a combination approach that equally or unequally weights each strategy.

By Anthony Chan4 months ago in Trader

How to Find the Best Freight Forwarder From China to the United States

As global trade becomes increasingly frequent, the demand for cargo transportation from China to the United States is increasing. Choosing a reliable freight forwarder can not only ensure the safe and timely delivery of goods but also save costs and improve efficiency for enterprises. This article will introduce in detail what a freight forwarder is, and explore in depth the best freight forward from China to the United States and the skills of selecting a freight forwarder.

By Bella Yang2 days ago in Trader

Confessions of an Empath

The birds are chirping, and the sun is shining in a cloudless July sky. The vibrancy promises a beautiful day, but the cooing of the Mourning Dove perched on the powerlines seems to be more fitting than the lively songs of the robin flitting through the trees. The melancholic calls of the dove cloak the world in a sadness that hangs like tattered drapes.

By Alyssa Nicoleabout 23 hours ago in Confessions

Comments

There are no comments for this story

Be the first to respond and start the conversation.