Mistakes to Avoid in Your 20s

How to Navigate your 20's and Avoid Deadly Money Mistakes

Intro

Your 20s are a time of exploration, growth, and newfound independence. While it's exhilarating to step into adulthood, it's also a crucial period for establishing healthy financial habits. Unfortunately, many young adults make common money mistakes that can have long-lasting effects. In this blog, we'll shed light on these pitfalls and provide insights on how to avoid them, ensuring you set a solid foundation for your financial journey ahead.

Neglecting the Importance of a Budget

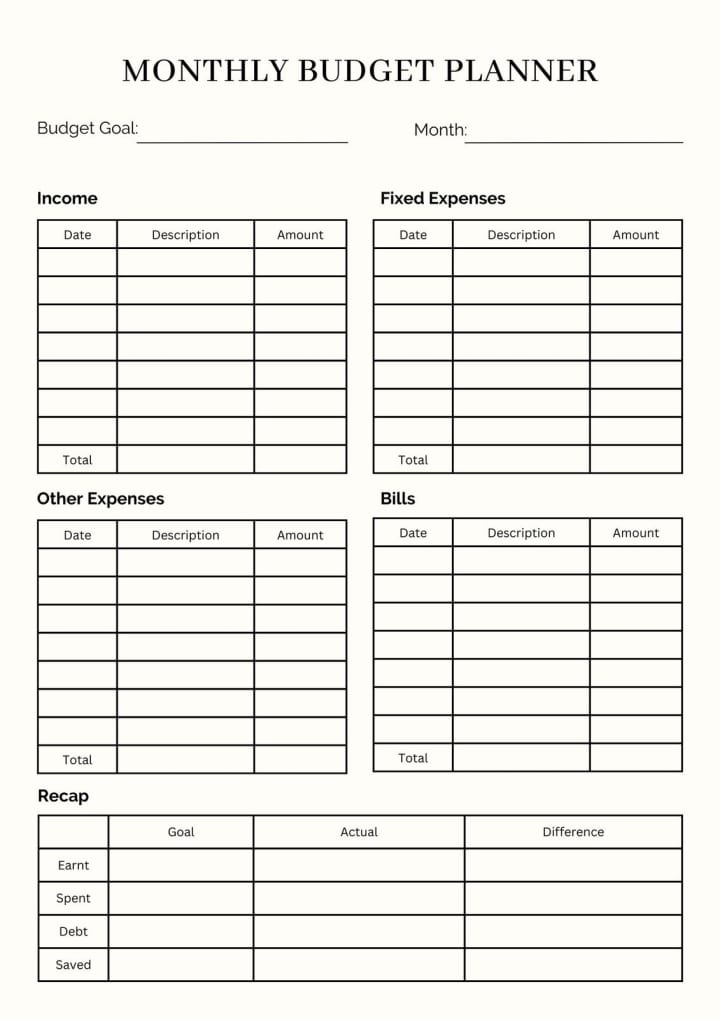

One of the most significant money mistakes in your 20s is not creating a budget. Failing to track your income and expenses can lead to overspending, debt accumulation, and missed financial opportunities. Start early by setting up a budget to understand where your money is going and allocate funds wisely.

A budget is essential because it empowers you with control over your finances. It provides a clear roadmap for your income, expenses, and savings, helping you allocate resources wisely. With a budget, you can track where your money goes, identify unnecessary spending, and prioritize essential expenses.

It acts as a safeguard against overspending, debt accumulation, and financial stress. Budgeting enables you to set and achieve financial goals, whether it's building an emergency fund, paying off debt, or saving for big dreams like a home or retirement. By creating a budget, you're making informed decisions, establishing discipline, and paving the way for a more secure and prosperous future.

Going Into Credit Card Debt

Credit cards can be convenient, but they also pose a danger of high-interest debt. Relying on credit cards without a clear repayment plan can quickly spiral into financial trouble. Use credit responsibly and pay off the balance in full each month to avoid interest charges.

Credit card debt can be detrimental due to its high-interest rates and potential to spiral out of control. The compounding interest on unpaid balances accumulates quickly, leading to an ever-growing debt burden. This debt can strain your finances, making it difficult to save, invest, or achieve financial goals. Credit card debt also negatively impacts your credit score, limiting your ability to secure favorable loan terms for future needs like buying a home or car.

It often reflects overspending and poor financial habits, hindering your financial well-being. Breaking free from credit card debt requires disciplined repayment and can take a toll on your mental and emotional health. To maintain financial stability, it's crucial to use credit cards responsibly, paying off balances in full each month and avoiding unnecessary high-interest debt.

Underestimating the Burden of Student Loans

While education is an investment in your future, student loans can become burdensome if not managed properly. Before taking out loans, explore scholarship options, part-time work, or community college to minimize the amount borrowed. Create a repayment plan to avoid long-term financial stress.

Student loan debt can pose a significant danger due to its potential to burden individuals with long-term financial stress. With the rising costs of education, borrowers often accumulate substantial debt that takes years or even decades to repay. This debt can hinder major life milestones such as buying a home, starting a family, or pursuing advanced degrees.

Moreover, student loans typically accrue interest, leading to a higher overall repayment amount. Unlike other debts, student loans are not easily discharged in bankruptcy, trapping borrowers in a cycle of repayment. Defaults on student loans can severely damage credit scores, limiting future financial opportunities. Thus, careful consideration of educational choices, scholarship opportunities, and repayment plans is essential to prevent the potential dangers of excessive student loan debt.

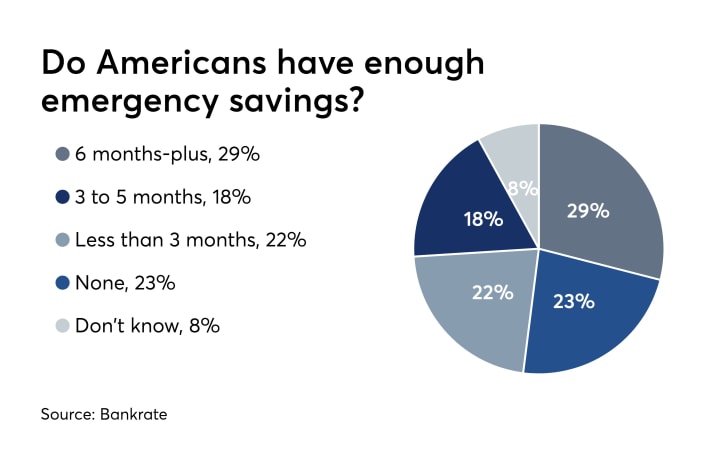

Not Building an Emergency Fund

Emergencies don't wait for the perfect financial moment. Failing to build an emergency fund can lead to resorting to credit or loans during unexpected situations. Aim to save three to six months' worth of living expenses as a safety net. Once again, this is something I discuss a bit in my article Things I've Learned in My 20's

An emergency fund is crucial for young adults as it acts as a safety net against unforeseen financial setbacks. Life's uncertainties, such as medical emergencies, job loss, or car repairs, can disrupt financial stability. An emergency fund provides immediate financial support without resorting to high-interest loans or credit card debt.

For young adults still establishing their careers, an unexpected setback can be particularly challenging. Having a well-funded emergency fund offers peace of mind, reducing stress and allowing them to focus on personal and professional growth. It's a foundational step toward financial independence, providing the confidence to navigate life's uncertainties and ensuring they can maintain their standard of living even during tough times.

There are two great resources that I personally use in building an Emergency fund. The first is Betterment, where you can get a cash reserve account with a daily compounding interest of 4.75%

The second is Sofi, which starts with 1.24% interest, but once you've linked a bank account and direct deposit, you unlock 4.45%. Personally, I would suggest you to go with Sofi, as Betterment's FDIC protections are selective and don't cover most cash reserve accounts.

Ignoring Retirement Savings

It's easy to overlook retirement planning in your 20s, but starting early has immense benefits due to the power of compound interest. Contribute to employer-sponsored retirement accounts and consider opening an Individual Retirement Account (IRA) for additional savings.

Starting to build your Individual Retirement Account (IRA) as soon as possible is crucial due to the power of compound interest and the extended timeline for growth. The earlier you contribute, the more time your investments have to grow exponentially. Even small contributions made in your 20s can accumulate into substantial sums by the time you retire. Starting early also allows you to weather market fluctuations and benefit from the average growth rate over a longer period, minimizing the impact of short-term volatility.

Additionally, contributing to your IRA offers potential tax advantages, reducing your taxable income in the present while securing your financial future. By beginning early, you're taking advantage of time as a valuable ally, setting the stage for a comfortable and secure retirement down the road. I breifly discuss the idea of savings and retirement funds in my article Things I've Learned In My 20's that has a few good resources and tips for savings.

Living Beyond Your Means

Embracing a lifestyle that your income can't support can lead to financial stress and debt. Avoid the trap of "keeping up with the Joneses." Instead, prioritize saving and investing over unnecessary expenses. Another problem is getting into the trap of Lifestyle creep.

Lifestyle creep, or "creeping inflation," refers to the gradual increase in spending as income rises. As earnings grow, individuals often upscale their spending on non-essential items, which can lead to inflated living costs, decreased savings, and hindered financial goals if not managed consciously.

Not Investing Early

Many young adults shy away from investing due to perceived complexities or risk. However, not investing means missing out on potential long-term growth. Start learning about different investment options and consult a financial advisor to make informed choices.

Investing early offers several compelling advantages that can significantly impact your financial future. The power of compound interest works in your favor when you start early, as your earnings generate more earnings over time. This exponential growth allows even modest investments to grow substantially over the long term. Early investing also provides a buffer against market volatility, allowing your investments to recover from potential downturns.

It instills financial discipline and encourages a long-term perspective, essential for building wealth. Furthermore, early investments enable you to take on more risk, potentially yielding higher returns, as you have a longer horizon to recover from any losses. By initiating your investment journey early, you're capitalizing on time as a valuable asset, maximizing growth potential, and setting the stage for a more secure and prosperous financial future.

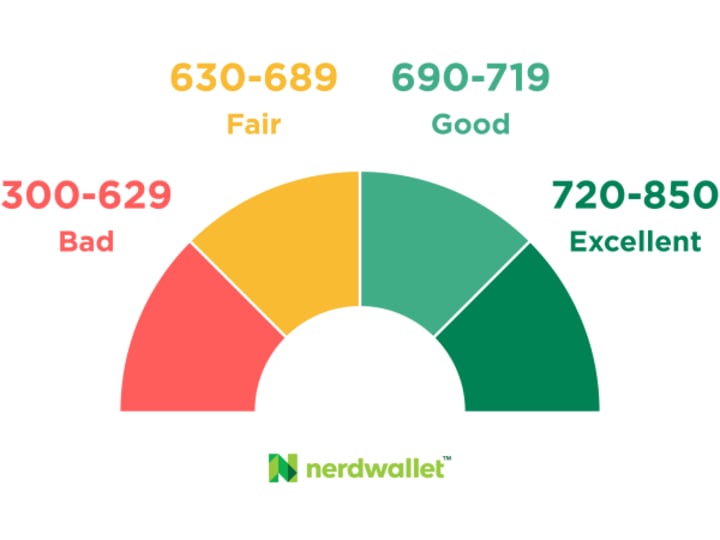

Failing to Build Credit

So, I know I just got done telling you how bad credit card debt is.. but you do need to be able to build GOOD credit. So... how do we do that?

A strong credit history is essential for future financial endeavors. Don't ignore credit-building opportunities, such as responsibly using a credit card or taking out a small loan. Aim to maintain a good credit score for better loan terms in the future.

Building good credit involves responsible financial habits. Start by obtaining a credit card and using it prudently; pay bills on time, ideally in full, to avoid interest. Keep credit utilization low, ideally below 30%. Monitor your credit report for errors and address them promptly. Diversify credit types, like having a mix of credit cards and installment loans. Maintain a longer credit history by not closing old accounts.

Be cautious about opening multiple new accounts in a short time. Responsible credit management over time establishes a positive credit history, boosting your credit score and enhancing your financial opportunities.

Neglecting Financial Education

Financial literacy is a lifelong journey. Ignoring the opportunity to educate yourself about personal finance can lead to missed opportunities and poor decision-making. Invest time in reading books, taking courses, and staying informed about financial news.

Neglecting financial education can lead to missed opportunities and poor financial decisions. Understanding personal finance empowers you to make informed choices about budgeting, saving, investing, and debt management. Without this knowledge, you might fall into debt traps, overspend, or miss out on potential investment gains. Financial literacy equips you to navigate economic challenges, plan for retirement, and secure your financial future.

It helps you recognize and respond to market trends and changing financial regulations. By investing time in learning, you gain the skills needed to assess risks, identify smart investments, and make strategic financial moves. Ultimately, financial education is an investment in yourself, arming you with tools to achieve your goals and attain financial independence with confidence.

Not Seeking Professional Advice

Navigating complex financial decisions without expert guidance can be risky. Engage with financial advisors or mentors who can provide personalized advice tailored to your circumstances and goals.

Seeking professional financial advice can be immensely beneficial due to the expertise and objective perspective it provides. Financial advisors possess specialized knowledge in areas like investments, taxes, retirement planning, and estate management, helping you make informed decisions aligned with your goals. They tailor strategies to your unique circumstances, ensuring your financial plan is optimized.

Advisors can navigate complex financial landscapes, minimizing risks and maximizing returns. They offer an unbiased viewpoint, helping you avoid emotional or impulsive choices. While self-education is valuable, advisors bring years of experience and up-to-date insights. Their guidance helps you establish a solid financial roadmap, adapt to changing circumstances, and stay on track to meet your short and long-term objectives with confidence.

Conclusion

Your 20s offer an exciting chance to lay the groundwork for a financially secure future. By avoiding these common money mistakes and adopting responsible financial habits, you can navigate the challenges of adulthood with confidence, setting yourself up for success in the years to come. Remember that every small step towards financial awareness and discipline today will lead to a brighter and more stable financial tomorrow.

About the Creator

QuirkyMin

Aspiring writer, sharing articles of personal interest as well as original short stories.

https://linktr.ee/quirky.min

Enjoyed the story? Support the Creator.

Subscribe for free to receive all their stories in your feed. You could also pledge your support or give them a one-off tip, letting them know you appreciate their work.

Keep reading

More stories from QuirkyMin and writers in Motivation and other communities.

Things I've Learned In My 20's

SAVINGS Did you know if you invest $1 into ETF's or an IRA in your 20's, by the time you retire it'll be around $80? But investing that same dollar in your 30's you'll only see around $45? Bottom Line: Your money in your 20's is just worth more. Or rather, the earlier you start saving and investing, the more that dollar will do for you.

By QuirkyMin3 years ago in Motivation

Savor the Flavor: The Enlightened Path to Weight Loss Through Mindful Eating

Keywords: Mindful Eating Techniques, Sustainable Weight Loss Strategies, Psychology of Eating, Conscious Consumption Habits, Mindful Eating Benefits, Exercise, Gym, Weight loss, Workout, Diet.

By ActiveVitaLifea day ago in Motivation

Americo Migliore: A Journey of Excellence

Intoduction Americo Migliore is not just a name in the interior stone and tile industry; he is a symbol of dedication, innovation, and unwavering commitment to quality craftsmanship. His career trajectory—from a hands-on field worker to a visionary leader—underscores his journey of excellence and the profound impact he has made on the industry.

By Americo Migliorea day ago in Motivation

Comments (1)

Way past my 20s but this is a very good list!